Starting January 1, 2026, Federal employees and retirees will be able to convert money from their traditional Thrift Savings Plan (TSP) accounts to a Roth TSP account. That is called a Roth in-plan conversion. Read the TSP announcement here.

This new feature gives TSP participants a tool that’s long been available for Roth IRAs but has been missing from the TSP: the ability to manage taxes proactively by shifting money into a tax-free growth vehicle. You don’t need an existing Roth TSP balance to do it — your first in-plan conversion will create one.

But just because you can convert doesn’t mean you should. That is because any amounts converted are fully taxable as ordinary income for the year they are made. TSP participants who convert are paying taxes early in order to reduce their future taxes. As a result, conversions will make sense for some TSP participants but not others.

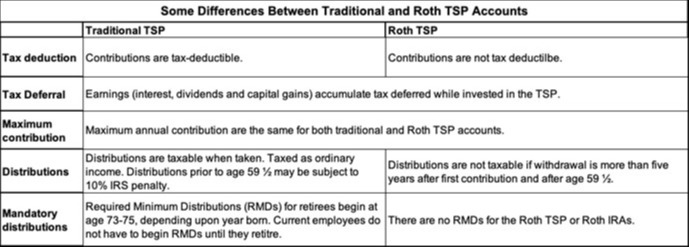

The Difference Between Traditional and Roth TSP Accounts

Federal employees can make their bi-weekly contribution to two types of TSP accounts – traditional (also called regular) and Roth. The government’s matching contributions always go to the employee’s tradtional TSP account.

- Traditional TSP:

Employee contributions to the Traditional TSP are pre-tax. That means the employee’s taxable income is reduced by the amount of the contribution. Earnings generated by the TSP funds are not taxed while the contributions remain in the TSP. However, withdrawals from the Traditional TSP are fully taxable as ordinary income. - Roth TSP:

Employee contributions to the Roth TSP are after tax; employees cannot deduct Roth contributions from their taxable income when calculating their taxes. However, Qualified withdrawals are tax-free and there are no Required Minimum Distributions.

For a withdrawal to be qualified, the participant must be older than 59 ½ (or permanently disabled) and the Roth TSP account must be more than five years old.

The only disadvantage to contributing to the Roth TSP is that the contribution is not tax deductible; it cannot be used to reduce your taxable income when calculating your tax payment. Contributions are “after-tax.”

In other respects, it is better to have money in the Roth than Traditional TSP:

- There are no Required Minimum Distributions

- Withdrawals are not taxed if qualified.

- Spousal beneficiaries and heirs do not have to pay tax on withdrawals.

Currently, neither employees or retirees can convert Traditional TSP balances to a Roth TSP account. Starting January 1 2026, both employees and retirees can convert any amount to a Roth TSP account.

How Roth In-Plan Conversions Will Work

Beginning in 2026, employees and retirees can instruct the TSP to transfer funds from their traditional TSP account to a Roth TSP account. The amount of the transfer is considered taxable income for that tax year.

Note that

- There is a $500 minimum for each separate conversion.

- The entire amount converted is treated as taxable income.

- The TSP will not withhold taxes on conversions.

- The TSP will report the taxable income to the IRS.

- The taxes must be paid with funds from a savings or taxable investment account.

- You cannot pay taxes using funds from the TSP or an IRA, unless you first withdraw the money and transfer to a taxable account, generating additional taxable income.

- The converted balance remains in the TSP, invested in the same funds with the same percentage allocation.

IMPORTANT: There are a lot of variables that affect whether a Roth conversion will be a good strategy.

Plan ahead. If you don’t have funds in a taxable account to pay the taxes, a conversion may not make sense.

When Roth Conversions Might Make Sense

A conversion might make sense when a TSP participant:

- Expects their tax rate to be higher in retirement. If the participants tax rate in retirement is expected to be lower or the same, a conversion probably does not make sense.

- Has cash on hand to pay the conversion tax.

- Wants to reduce future RMDs from their traditional TSP account.

- Wants to leave tax-free money to heirs.

- Is an aggressive investor expecting high growth — the bigger the gains, the more benefit to tax-free treatment.

- Does not expect the funds in the Roth account to be needed for a long period of time.

- Want to lower Medicare premiums by reducing taxes on future withdrawals.

A conversion may not make sense when a TSP participant:

- Is currently in a high tax bracket.

- Is subject to the Net Investment Income Tax.

- Needs the money within the next 5–10 years. Conversions take time to pay off.

- Is 75+ and already taking RMDs.

- Doesn’t have funds outside the TSP to pay the taxes.

Mathematically, if a participant expects their tax rates to be lower or the same in retirement, a Roth conversion is probably not beneficial. But for participants who expect their retirement tax rate to be higher, it could pay off — especially for long-term, growth-oriented investors.

Final Thoughts: Who Should Consider This?

Congratulations to the TSP for offering another option. But this option is not for everyone; it can backfire without careful planning. Participants should ask a financial planner or tax advisor to help them decide whether it makes sense. The TSP has wisely emphasized this. The wrong decision can cost more in taxes than it saves and reduce the future after-tax value of investments.

Please contact us if you need help making this decision.