Third Quarter Investment Commentary

Following negative returns in the first quarter, markets have been strong in the second and third quarters.

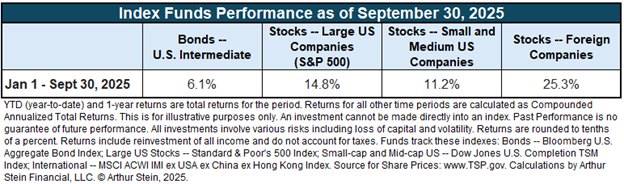

As of the end of the third quarter, US stocks (the S&P 500) are up about 15% year-to-date while International stocks (the MSCI All Country World Index ex US) are up about 25%. That included an S&P 500 decline of almost 20% earlier in the year but both indexes are up about 33% since the April 8th market bottom.

US bonds (the Bloomberg US Aggregate Bond index) also performed well and are up about 6% year-to date; their best start to a year since 2020.

Second quarter GDP (released in the third quarter) increased at a 3.8% annualized rate. The GDP growth was driven by strong consumer spending, flat government spending, and a reduction in imports.

The economic picture is always uncertain but the developments of post-Covid normalization, the significant inflation and subsequent disinflation, changing US fiscal policy, geopolitical events globally, and the early stages of the AI super-cycle have made the complexity feel more acute than in most periods.

As always, markets react to current perceptions of positive and negative trends.

Positive factors included:

- Strong GDP growth as mentioned above and expectations for similar GDP growth of 3.5%- 4% annualized for the third quarter (as of this writing).

- Optimism about AI development and adoption and the related infrastructure buildout.

- A Federal Reserve rate cut, and more cuts expected by the end of the year. The Fed cut rates by one quarter of one percent in September, its first rate cute since December 2024.

- Lower mortgage and Treasury rates.

- Lower oil prices.

Negative factors included:

- A slightly higher, though still low unemployment rate.

- A frozen labor market: hiring rate, quits rate, initial unemployment claims, and growth in job openings are muted.

- Relatively sticky inflation. Inflation remains above the Federal Reserve’s 2% year-over-year target. Although inflation has come down substantially, it remains sticky at around 2.5% - 3%.

- Concern about global debt, deficit levels, and geopolitics.

2025 has clearly been a good year for investment assets. The table below shows the total return of Bonds, US stocks (of large & medium/small market capitalizations), and international stock indexes.

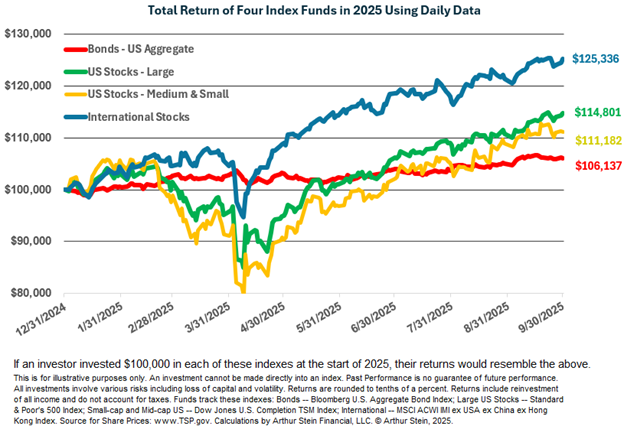

This strong performance hides the volatility investors saw earlier in the year. The chart below shows the fluctuation in these indexes over the same year-to-date period.

The S&P 500 Index declined about 19% between mid-February and the first week in April. That is just short of a Bear Market decline of 20% or more.

Since then, the markets have benefited from lower interest rates, clarity on fiscal policy, reduction in regulation, significant private sector investment, M&A activity, and various other factors.

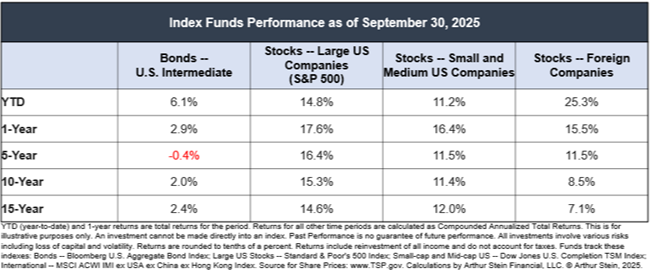

Over longer periods of time (such as the 10 & 15 year returns shown below):

- Stocks of large U.S. companies outperformed small and medium sized U.S. companies

- Both U.S. stock indexes outperformed the foreign stock index

- The stock indexes significantly outperformed the bond index.

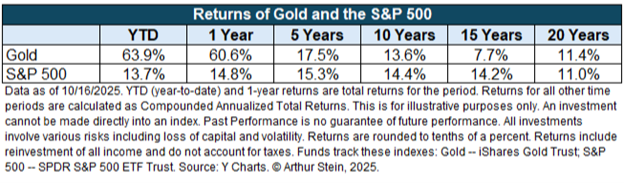

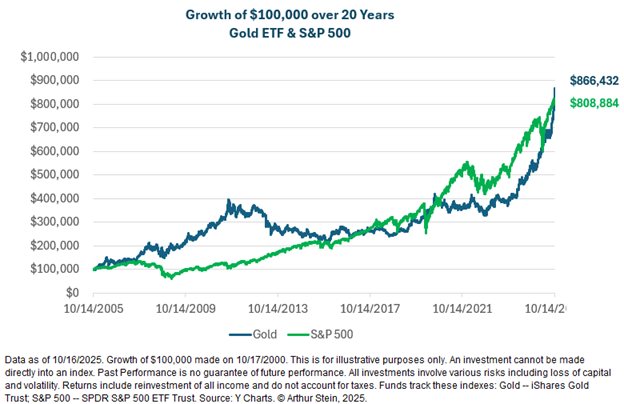

Gold has received a lot of attention recently because of strong performance. However, the S&P 500 returns over the last 15 years were twice the performance of gold. There has been increasing interest and investment in gold for multiple reasons (many of which are complex) but mainly due to the ideas of devalued fiat currencies and the changing geopolitical order. Most countries around the globe are facing rising debts, persistent deficits, and worsening demographics. Attempts to reduce fiscal spending and deficits faced significant pushback in the US and Europe. Since money printing doesn’t show signs of slowing down globally, hard assets such as gold became more attractive.

Earlier in the year, we received questions from some clients asking if changes should be made to the allocations of their Portfolios. Although we review each client’s financial situation independently, we generally did not make major changes to the Portfolio. We are glad we didn’t.

Reducing stock allocations because of stock market declines would have meant missing out on strong second and third quarter returns. In fact, our philosophy is the opposite: when stocks decline enough that your Portfolio is under-invested in stocks according to the agreed upon asset allocation, we rebalance the Portfolio and buy stocks at lower prices.

The returns went to those investors who stayed disciplined and waited out the choppy market experience. We are buy-and-hold, disciplined investors. We don’t move in or out of financial markets in anticipation of some future change. Historically, frequent trading and predictions did not lead to increased profitability. Of course, past performance is no guarantee of future performance.

At Arthur Stein Financial, we stick to a strategy designed to weather a wide variety of market conditions. Our approach emphasizes:

- Diversification: Your investments are spread across 21 funds from 18 different fund companies covering broad and diversified asset classes.

- Long-term perspective: We don’t try to predict short-term moves. We stay focused on your goals and maintain a disciplined approach.

- Volatility management: We aim for good long-term returns with less risk and volatility, not the highest possible returns.

- Cash flow planning: We work with you to ensure your expected withdrawals are covered, so you don’t need to sell during a downturn.

- Tax efficiency: We look for opportunities to reduce your tax burden, especially during rebalancing.

If you’re feeling unsettled or just want to talk things through, please reach out. We’re here to help—now and always.

Disclaimers:

This is for educational purposes only. To learn more about the topics mentioned and if they are suitable for you, consult an appropriate professional. Tax laws can change at any time.

Any information provided in this presentation has been prepared from sources believed to be reliable but is not guaranteed and is not a complete summary or statement of all available data necessary for making an investment decision. Any information provided is for information purposes only and does not constitute a recommendation.

Arthur Stein and Arthur Stein Financial, LLC are not authorized to give legal or tax advice. For information on your specific situation, please consult your tax advisor regarding any tax implications and your attorney for legal implications. As required by the US Treasury Regulations, you should be aware that this presentation is not intended to be used and it cannot be used for the purposes of avoiding penalties under federal tax laws.

Keep in mind that:

- Past performance is no guarantee of future performance;

- Investments involve the risk of loss of principal and earnings;

- ETFs, mutual funds, money market funds, etc. are not guaranteed by the US Government, the FDIC, a bank or anyone else.

- “Average annual return” evens out variations in the actual year-to-year returns.

- ETFs, mutual funds and individual stocks and bonds fluctuate in value and there will always be times when they lose value.

- None of the information provided is necessarily relevant to anyone’s personal situation. Circumstances differ among individuals and you should not assume that these generalizations or information apply to you.

- Investments mentioned may not be suitable for all investors.

- An investment cannot be made directly into an index.