We have received some questions from clients about whether an increased allocation to International Stocks is warranted given US tariff policy, a weakening dollar, and relative valuations.

In this piece, we will list some of the reasons why International Stocks have generated more interest, provide context about these reasons, discuss the relative merits of investing in both US and International Stocks, and provide a reminder of your Portfolio’s diversification and the benefits of that strategy.

Why Have International Stocks Generated More Interest Lately?

1. Claims that “American Exceptionalism” has been Weakened.

Allocating investments is a relative endeavor. Inherent in the idea that International Stocks are more attractive is a correlated notion that US Stocks are therefore relatively less attractive. But is that the case?

American Exceptionalism is a broad concept that generally refers to the idea that the United States provides unique advantages and opportunities for investment returns due to its strong economic framework, its housing of the best and most innovative companies, its consistent rule of law, its deep and robust capital markets, and its reserve currency status.

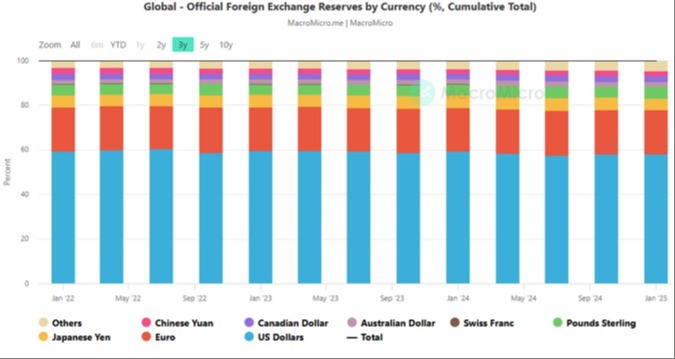

The argument would go that some of these factors may be weakening. The one pointed to most frequently is the idea of the US losing its status as the global reserve currency.

While the dollar has in fact weakened against most other currencies so far this year (more on that below), its share as a percentage of reserve currencies has not changed (blue bars).

Additionally, some people point to trade policy and tariffs as a reason that the US is a less attractive place for investment.

There is a wide range of opinions on what the effect of tariff policy will be. While tariff rates and trade deal details change frequently, the administration has been clear in its overarching beliefs with regard to tariff policy:

a) that the US has been getting ripped off because US trade policy has historically allowed foreign companies to sell products in the US with no trade barriers while other countries apply tariffs and non-tariff trade barriers to US companies selling into their markets.

b) that these uneven trade policies have hurt domestic US firms by being less competitive on the global market, and that by raising tariff barriers, domestic industries will thrive by increasing US manufacturing and business formation. And,

c) that tariff policy will not be inflationary for the US consumer.

As mentioned above, we don’t yet know what the final results of these policies will be but there are some positive early indications that has softened some of the early hysteria.

Whether or not the US has been getting “ripped off” is up for debate and both sides of that view have fair arguments. Tariffs are not new but are clearly a bigger priority for this administration.

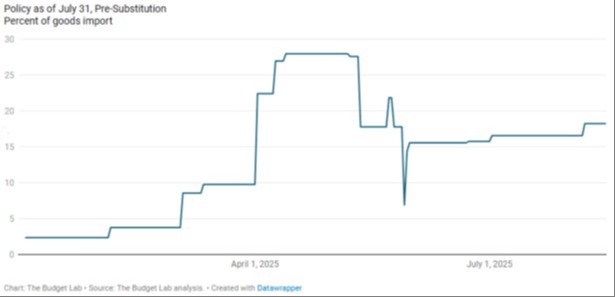

The effective tariff rate was about 3% coming into 2025 and stands around 17% as of this writing, although that number will likely change.

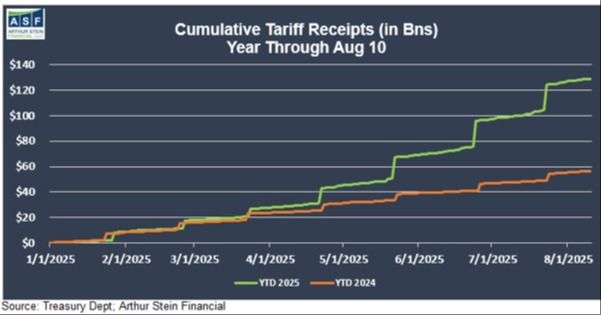

The effect of that has been a significant increase in customs revenue entering the US. That revenue can be used to pay for general expenses, pay down the debt, and/or to provide direct payments to citizens.

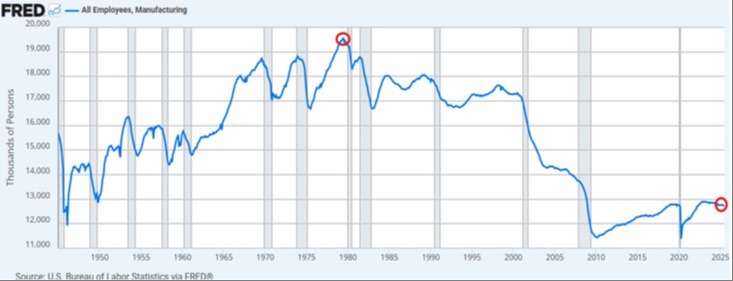

It is impossible to argue that manufacturing has become a smaller part of the US economy due to some combination of globalization and the economic transition from a goods economy to a services economy. How important that is for the US is another debate, and probably largely depends on where you live and what line of work you are in.

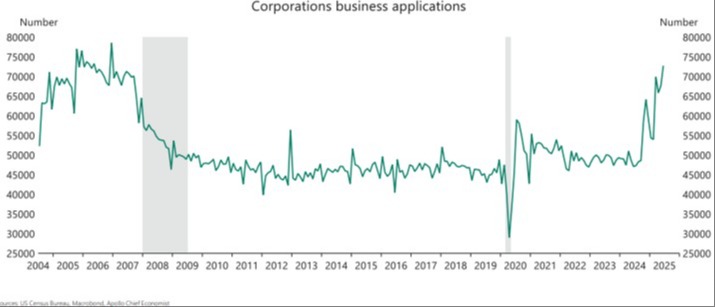

So far, US business formation has remained robust as shown in the second chart. It stands to reason that this will continue as domestic businesses become relatively more attractive on a global scale, but a recession would likely stall this trend.

Whether tariff policy will be inflationary is probably the biggest debate underway. Some argue that tariffs will be massively inflationary and others argue the US consumer will experience virtually no sustained inflation.

The truth is that no one knows. So far we have not seen a material increase in inflation to US consumers but it is possible that affects are lagged. My personal view is that the total cost will be spread between several parties along the supply line with each taking a partial, but not necessarily equal, share.

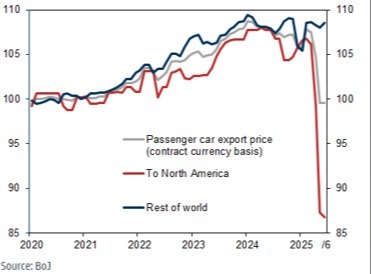

For example, if a Japanese automaker is shipping a car to the US, the following parties will pay some part of the tariff: the Japanese automaker, the Japanese distributor, the shipping company, the US port, the US importer, and the US consumer.

There is some evidence that this is the case (shown below) but the ultimate outcome is unknown.

So with all that in mind, its necessary to evaluate the effects on foreign countries and see how their economies are doing. Since “foreign companies” refers to everything other than the US, we can’t and wouldn’t want to evaluate all of them but we will check on a few major geographies to provide more context on the relative attractiveness of US vs International investment.

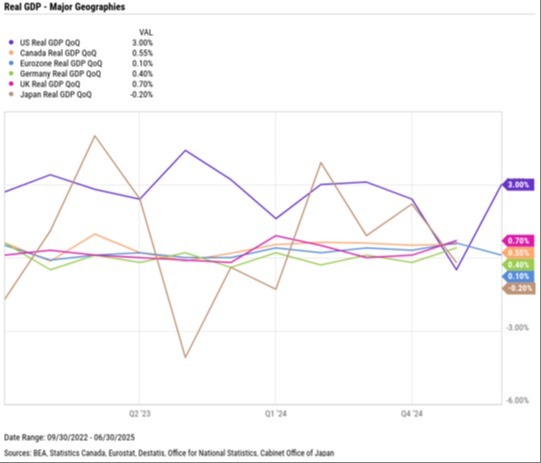

The economies of other major geographies appear sluggish. The chart below showing GDP figures for major global economies shows the US experiencing far better growth than the others. The Atlanta Fed is forecasting third quarter US GDP at 2.5%.

I recently read a stat from Brent Donnelly at Spectra Markets that said that Microsoft’s fiscal 2025 profit is as high as the profits of the 50 largest Canadian companies combined. I haven’t independently verified that but I would not be surprised.

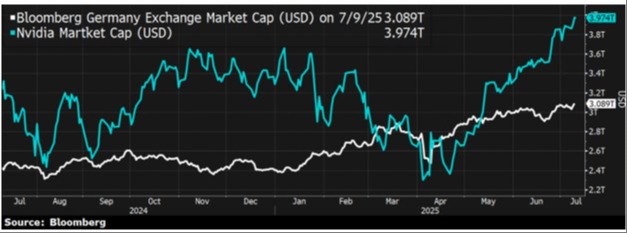

Furthermore Nvidia, the largest US company by value, has a higher valuation than the entire market capitalization of Germany, Europe’s economic engine. Note that this chart is about a month old and Nvidia’s market cap has increased from $3.9 trillion to $4.5 trillion. It reminds me of the saying: “the US innovates while Europe regulates”.

All of this is to say that allocating investment resources toward International Stocks requires the belief that foreign markets are a relatively more attractive place to invest than the US. While other countries and stocks of companies in those markets certainly have the potential to grow and perform well, it is usually difficult to successfully bet against the US economy.

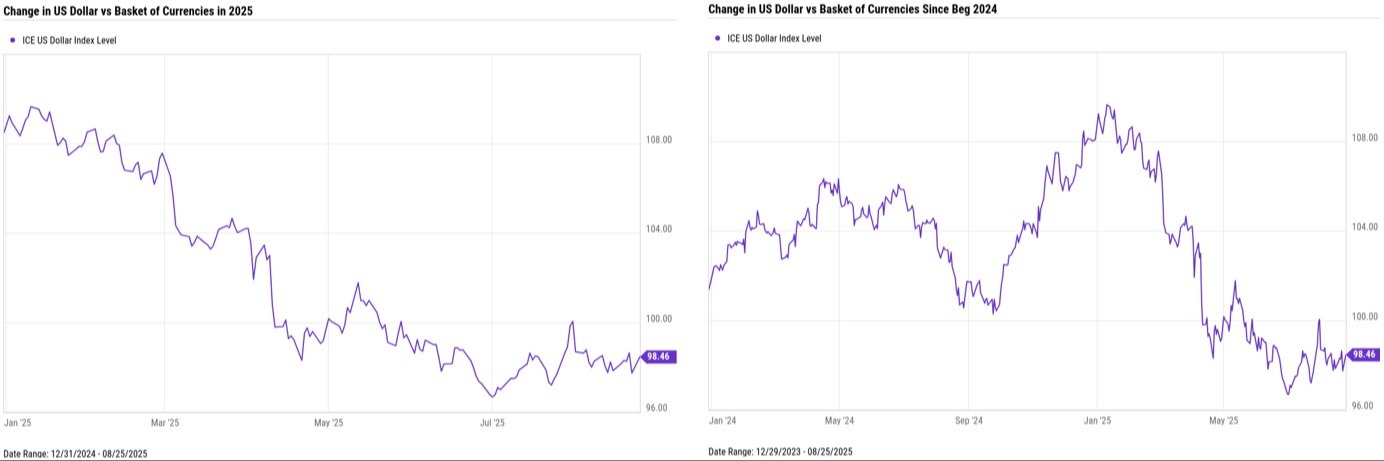

2. A Weakening US Dollar

Returns on investments of foreign companies by dollar based investors increase when the US dollar weakens, all other things even. As a result, people have pointed to a weakening dollar as another reason for increased consideration of International Stocks.

The global currency market is complex and currency values fluctuate for a variety of reasons including, but not limited to: relative inflation, interest rates, and trade. Using a simple example, if people sell Dollars to buy British Pounds, the dollar weakens and the Pound strengthens.

The strength of other currencies relative to the US dollar has provided a tailwind for International Stock returns so far in 2025. But to provide historical context, the decline in the dollar relative to other currencies is not severe when looking back to the beginning of 2024. See both charts below.

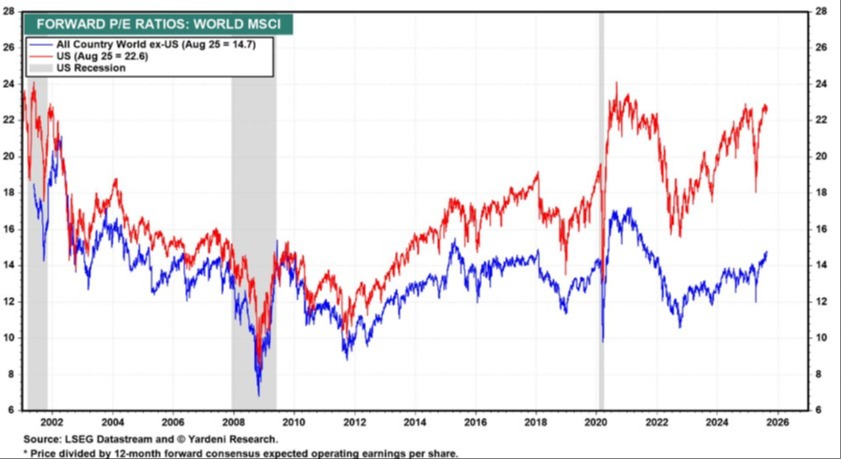

3. Stocks of Foreign Companies are “Cheap”

This is in reference to the price-earnings (P/E) ratio, or P/E multiple, which refers to how much an investor is willing to pay now for each dollar of a company’s future projected earnings.

As shown below, it is true that International Stocks (blue line) trade at a lower P/E multiple than US Stocks (red line). Therefore they are “cheaper” on this measure.

Forward Price to Earnings Multiple of International Stocks (blue line) and US Stocks (red line):

US P/E multiples are generally higher than those of other countries because US companies are expected to deliver higher growth, more durable profits (think iPhones, Microsoft Excel, etc), operate in a stronger economic environment, and benefit from higher investor sentiment and risk appetite.

In theory, a lower starting valuation should mean better forward returns. Most people want to buy something of good value for a lower price.

This has been a narrative for many years. I can recall several years of outlooks from Wall Street strategists calling for higher International Stock returns due to the relatively low valuation. But that has not come to fruition prior to this year.

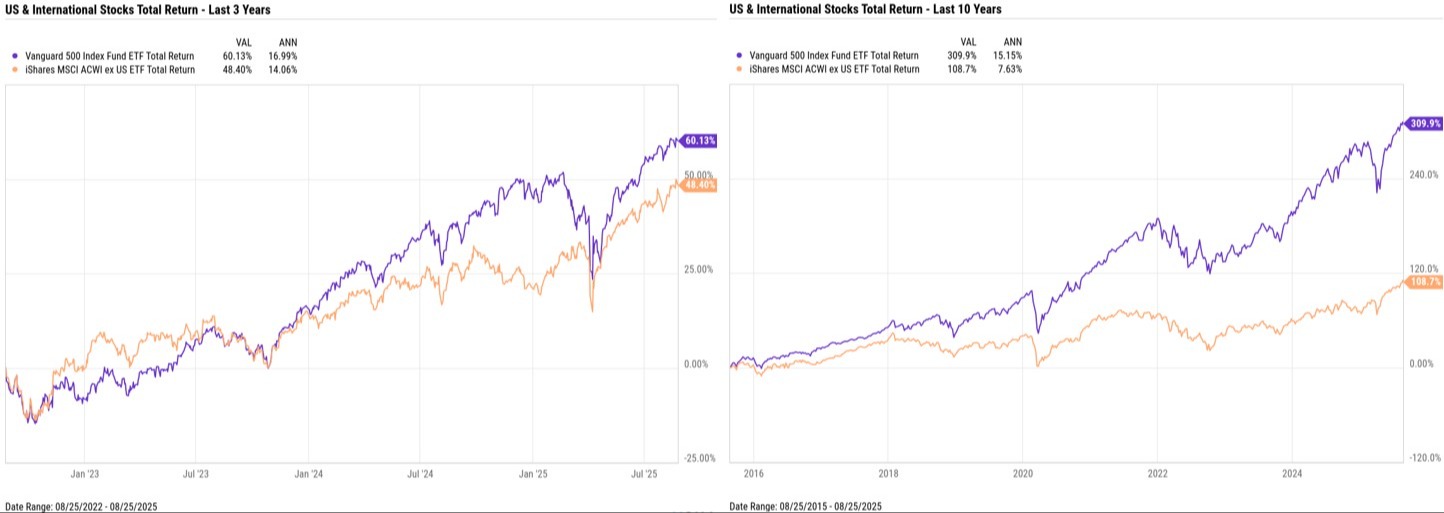

So far this year International Stocks (as measured by the All Country World Index ex-US) has doubled the return of US Stocks (as measured by the S&P 500). International Stocks are up about 22% while US Stocks are up about 11%.

But as with all things, context matters. Zooming out, the trailing 3 and 10 year returns of the US Stock market (purple line) have dominated International Stock returns (orange line) despite the relative strength of International Stocks this year and the historical discount of International Stocks.

3 and 10 Year Total Returns of the US Stock Market Index (Purple Line) & the International Stock Market Index (Orange Line):

Historically, we have seen long periods of US outperformance followed by long periods of International outperformance and vice versa - so that trend may be in the process of unfolding. But lower valuations of International Stocks compared to US Stocks is not a new concept and has not led to better returns over this period.

What Does This Mean for Your Portfolio?

When constructing your investment Portfolio, we believe in diversification of investment risk. The Portfolio we manage for you at Schwab owns assets of loans (Bonds) and ownership stakes (Stocks) according to the asset allocation that we’ve agreed upon.

It contains funds that own securities of US companies and non-US companies; stocks of growth companies and value companies; stocks of large companies and small companies, etc.

Your Portfolio has meaningful investments in both US and non-US Stocks so the diversification enables a spreading out of investment risk and allows the Portfolio to benefit from US and International Stocks rising in value with the understanding that one may outperform the other for some period of time.

Diversification also allows us to rebalance the Portfolio when one asset class or another is outperforming. It provides a smoother ride with less volatility than if all investment risk were concentrating into one basket.

Conclusion

It is understandable that International Stocks have garnered more interest than usual because of changing US trade policy, a weakening dollar, relative valuation, and the historical rotation of market leadership between US and International Stocks.

As we reviewed above, context matters and predictions of future events – both bullish and bearish – are rarely both accurate and timely.

Instead of trying to predict which areas of the market will outperform others over a given period, we maintain a diversified Portfolio that stands to benefit regardless of which areas of the market outperform with a disciplined rebalancing strategy that takes advantage of these moves.

When one geography outperforms the other, your Portfolio benefits from the return of that geography and provides us with the opportunity to sell high and rebalance the Portfolio to its target allocation.

Disclaimers:

This is for educational purposes only. To learn more about the topics mentioned and if they are suitable for you, consult an appropriate professional. Tax laws can change at any time.

Any information provided in this presentation has been prepared from sources believed to be reliable but is not guaranteed and is not a complete summary or statement of all available data necessary for making an investment decision. Any information provided is for information purposes only and does not constitute a recommendation.

Arthur Stein and Arthur Stein Financial, LLC are not authorized to give legal or tax advice. For information on your specific situation, please consult your tax advisor regarding any tax implications and your attorney for legal implications. As required by the US Treasury Regulations, you should be aware that this presentation is not intended to be used and it cannot be used for the purposes of avoiding penalties under federal tax laws.

Keep in mind that:

· Past performance is no guarantee of future performance;

· Investments involve the risk of loss of principal and earnings;

· ETFs, mutual funds, money market funds, etc. are not guaranteed by the US Government, the FDIC, a bank or anyone else.

· “Average annual return” evens out variations in the actual year-to-year returns.

· ETFs, mutual funds and individual stocks and bonds fluctuate in value and there will always be times when they lose value.

· None of the information provided is necessarily relevant to anyone’s personal situation. Circumstances differ among individuals and you should not assume that these generalizations or information apply to you.

· Investments mentioned may not be suitable for all investors.

· An investment cannot be made directly into an index.