Checking in on the US Consumer

The US consumer has been on a rollercoaster the last few years. They have endured the economic shutdowns during Covid, the stimulus and demand driven post-pandemic boom, four-decade high inflation, and rapidly rising interest rates – all in a short period of time.

The post-Covid economy has been difficult to understand. Some measures point to a healthy, robust consumer capable of maintaining spending. Others show cause for alarm. You could ask two different people how they think the economy is doing and get two completely different answers.

Let’s check on the US consumer by looking at the data.

Why Does Consumer Data Matter?

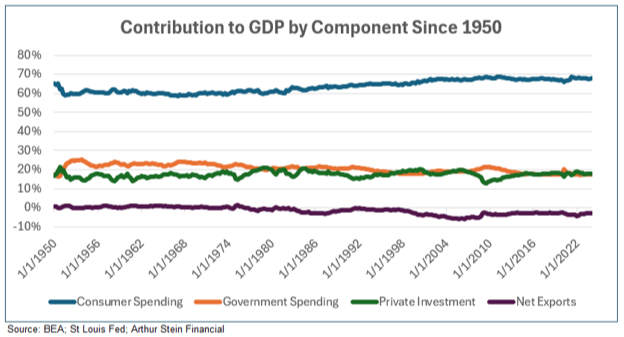

Consumer spending comprises about 70% of US Gross Domestic Product (GDP) and has always been the leading driver of GDP. As a result, the US economy relies on the health and trends of consumer spending. In other words: as the consumer goes, the economy goes.

The Consumer Income Statement

Income minus Spending = Savings. We will not address taxes but that is another “expense” people must pay before they can turn earnings into savings.

Income

Nominal wages, salaries, and income have increased steadily over time but range widely between the lowest earners and top earners.

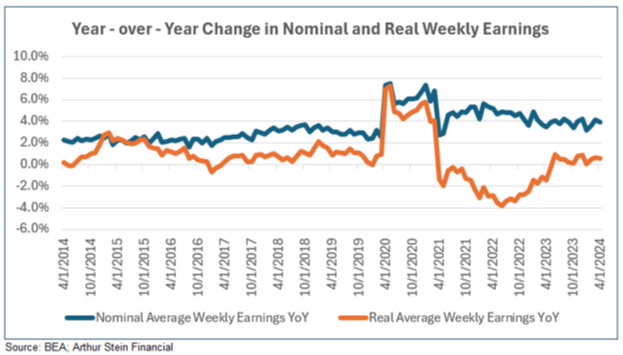

However, we know that inflation reduces the purchasing power of income and savings. The table below shows the nominal (before-inflation) and real (after-inflation) year-over-year change in average weekly earnings over the last 10 years.

Real wages (in orange) were negative for about two straight years from April 2021 to May 2023. This means that people (on average) fell behind for an extended period of time. Fortunately, as the rate of inflation has come down, real earnings have been positive for about a year.

Spending

Consumer spending has been strong but some cracks have emerged recently.

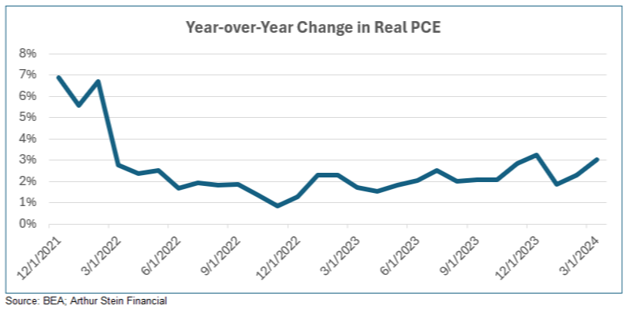

The two primary ways to measure consumer spending are Real Personal Consumption Expenditures (Real PCE) and another called Retail Sales. Real PCE measures the value of the goods and services purchased by U.S. residents and includes goods as well as things like healthcare, rent, and insurance. Retail Sales measures spending at a variety of retail locations including auto dealers, bars & restaurants, clothing stores, gas stations, and others.

PCE has remained strong, growing about 2-3% for much of the last year or so.

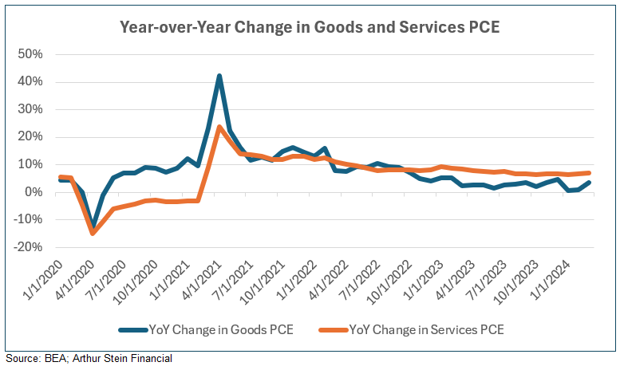

Interestingly, the composition of consumer spending has changed drastically over the last few years.

During Covid, spending on goods was the primary driver of spending, but spending on services has been the favored category since then.

This makes sense as people bought goods (physical things like TVs, laptops, and couches) while stuck at home. When the economy re-opened, spending moved toward services (such as airfare, dining out, and sports and concert tickets). It has remained that way for some time as growth in services spending has been higher than growth in goods spending for 18 straight months.

Meanwhile, nominal (before-inflation) Retail Sales have been quite strong as consumers spend and prices have gone up. However, real Retail Sales (after-inflation) have actually been trending sideways/negatively for about 3 years now.

Additionally, the year-over-year change in real Retail Sales has been negative for most of the last year.

Finally, Corporate America has been mentioning signs of a slowdown on its first quarter earnings calls. Companies like Starbucks, McDonalds, Yum Brands, and others have said that they see consumer spending tightening.

These may be signs that consumers are starting to pull back on spending.

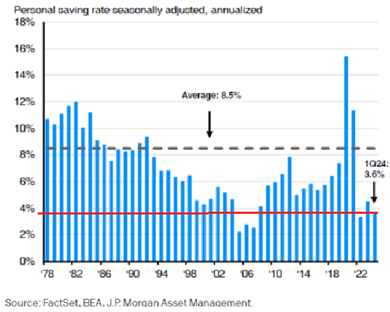

Savings

In aggregate, the savings rate among US consumers is at one of its lowest levels in the last 50 years and well below average. Although savings levels were high during the Covid-era, the savings rate has dropped back near the lows of 2022.

So, real wages have not been particularly strong and savings are coming down, yet most spending figures look solid. How do consumers continue spending?

For many people, through debt.

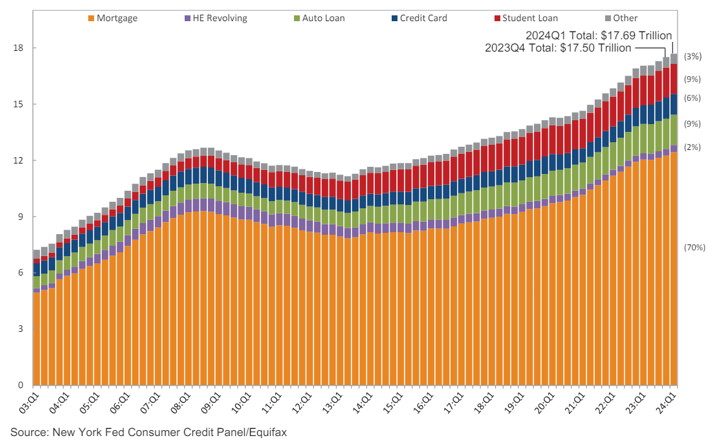

Consumer Debt

Americans have a lot of debt. That is not necessarily a bad thing because having a mortgage on a house or taking out a loan to pay for a car enables people to utilize their asset now while paying for it over time. Debt only becomes an issue when debt payments can’t be paid for with income or modest savings withdrawals.

Each quarter, the New York Fed puts out the Household Debt and Credit Report which contains valuable insights to consumers debt levels.

As of the end of the 1Q24, consumers held $17.69 trillion in debt, mostly through mortgages.

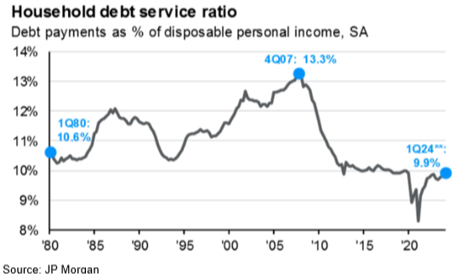

As a group, households have the ability to pay these debts. When interest rates were at historic lows, many Americans refinanced or purchased a home at very low mortgage rates which keep debt servicing costs manageable. The percentage of disposable income that goes toward debt payments (measured by the debt service ratio below) is near historic lows, although it has trended higher recently.

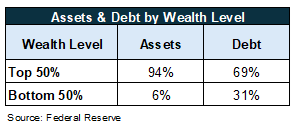

However, the aggregate does not tell the entire story.

One thing to note is that individuals in the bottom 50th percentile of wealth own only 6% of the assets, but they hold about a third of the debt and a high portion of that debt is credit card and auto loans.

Many assets have appreciated significantly in value: home prices have risen considerably and many stock markets are near all-time highs. Therefore, those with assets and savings have done very well, while those without assets and carrying variable rate debt have struggled.

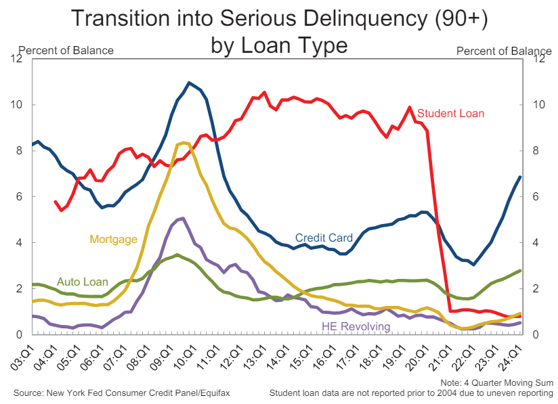

The real concern can be seen in the Delinquency data.

As of 1Q24, about 1 out of every 12 auto loans and 1 out of every 11 credit card loans have fallen into delinquency. Unlike mortgages, these loans tend to be shorter (auto) and variable rate (credit card) which leaves the borrower exposed to higher rates.

More concerning is the rapidly increasing rate of credit card debt that is severely delinquent.

Unless the holders of this seriously delinquent credit card debt pay off or re-finance their loans soon, millions of people will need to file for bankruptcy.

Unsurprisingly, younger individuals (18-39) and poorer individuals (bottom 50% of income) are experiencing serious delinquency more acutely.

How is the Consumer Feeling?

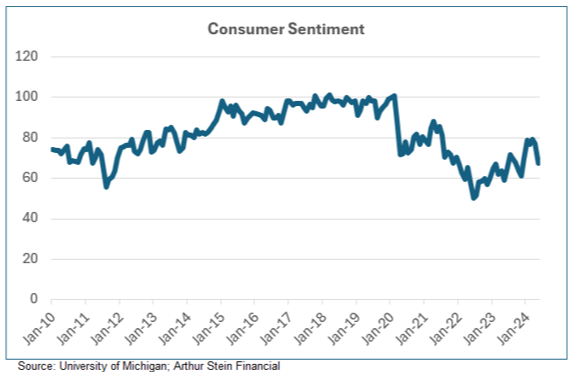

Survey data have varying degrees of reliability and some are better than others, but let’s see how consumers have been reporting their confidence and sentiment. The University of Michigan has been polling consumers since the 1940s.

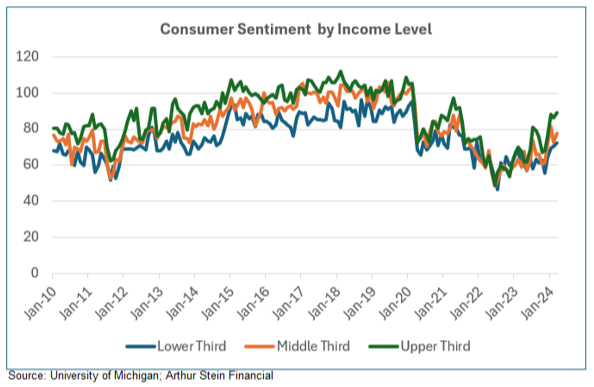

Overall, consumer sentiment has increased since 2022 but is still well below pre-Covid levels and has started to decline during the last few months. Sentiment by income level diverges quite a bit with poorer people reporting less favorable sentiment.

Conclusion

This has been a notably difficult economic environment to understand and it remains difficult to get a good sense of the state of the US consumer.

Many economists and pundits have predicted a recession and a slowdown for the consumer due to higher inflation and interest rates than consumers have been used to. We haven’t seen that in a major way so far.

To determine whether or not the consumer is in good shape, it may depend on which consumer.

Based on the data, the consumer appears to be resilient in the aggregate. However, lower- and middle-class consumers clearly appear to be struggling and are increasingly resorting to debt that they can’t pay to make purchases.

It’s most appropriate to think of this economy as one that is being held up by consumers in the top half of the income bracket while the lower half may be falling behind.

Disclaimers:

This is for educational purposes only. To learn more about the topics mentioned and if they are suitable for you, consult an appropriate professional. Tax laws can change at any time.

Any information provided in this presentation has been prepared from sources believed to be reliable but is not guaranteed and is not a complete summary or statement of all available data necessary for making an investment decision. Any information provided is for information purposes only and does not constitute a recommendation.

Arthur Stein and Arthur Stein Financial, LLC are not authorized to give legal or tax advice. For information on your specific situation, please consult your tax advisor regarding any tax implications and your attorney for legal implications. As required by the US Treasury Regulations, you should be aware that this presentation is not intended to be used and it cannot be used for the purposes of avoiding penalties under federal tax laws.

Keep in mind that:

Past performance is no guarantee of future performance;

Investments involve the risk of loss of principal and earnings;

ETFs, mutual funds, money market funds, etc. are not guaranteed by the US Government, the FDIC, a bank or anyone else.

“Average annual return” evens out variations in the actual year-to-year returns.

ETFs, mutual funds and individual stocks and bonds fluctuate in value and there will always be times when they lose value.

None of the information provided is necessarily relevant to anyone’s personal situation. Circumstances differ among individuals and you should not assume that these generalizations or information apply to you.

Investments mentioned may not be suitable for all investors.

An investment cannot be made directly into an index.