Many financial markets hit record highs in the first quarter of 2024. For example, large US stocks (as measured by the S&P 500), Japanese stocks (as measured by Nikkei 225) and Bitcoin (the speculative cryptocurrency) all hit record highs.

The Good and Bad News

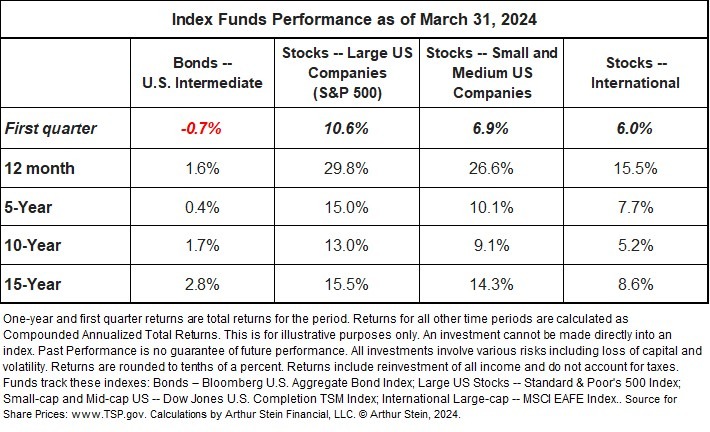

The S&P 500 Index of stocks of large US companies hit a record high late in January, leading to its best first-quarter performance since 2019. The Federal Reserve provided encouraging news following its meeting in March as it projected three interest rate cuts by the end of the year (although that now seems in doubt). Ten of the 11 S&P 500 market sectors posted quarterly gains, with industrials, information technology, communication services, financials, and energy climbing more than 10.0%.

Markets were encouraged by strength in the economy, high job creation, low unemployment, lower inflation, solid earnings, strong consumer spending, expectations for interest rate cuts and opportunities in artificial intelligence.

Better-than-expected workforce and productivity gains are behind the U.S. economy’s continued vigor. Household balance sheets were bolstered by pandemic-related fiscal policy and a virtuous cycle where job growth, wages, and consumption supported one another. While economic growth has fallen or stagnated in many other developed countries, US growth remains strong.

Of course, there was also plenty of bad news:

- Crude oil prices increased as oil exporting countries cut back on supplies and international conflicts continued. Gas prices increased because oil prices increased.

- Interest rates rose in the quarter, which hurt the bond markets. Bond market returns were negative in the first quarter and continued to lag stocks.

- Home mortgage rates remained high.

- Worldwide tensions and problems remain high and, in some cases (the Middle East), have increased.

- Finally, large company stock valuations are high and market concentration remains a concern.

Inflation

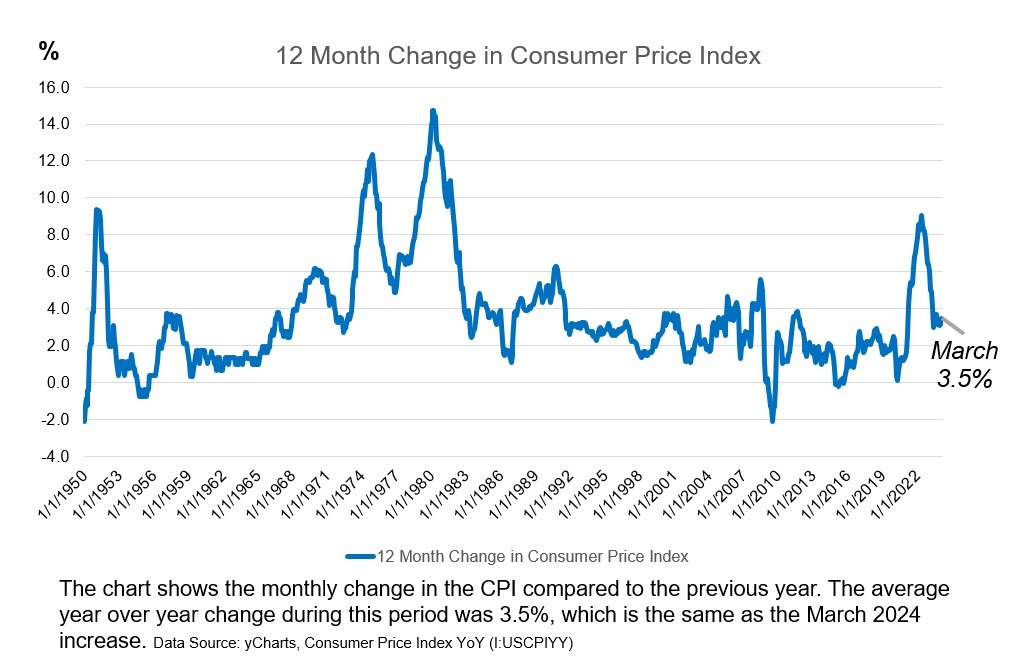

Many commentators and politicians add too high inflation as additional bad news. Well, no. Inflation jumped during 2022 and into 2023 but has since moderated to a level that is close to the average US inflation rate (1950 through March 2023) of 3.5%. See the chart below.

The inflation “problem” isn’t the current level, it is the cumulative inflation from the last few years, the loss of purchasing power by many groups (income not going up enough to increase or maintain purchasing power) and the use of inflation as a political weapon.

Although the annual rate of inflation has slowed since its 2022 peak, inflation is still well above the Federal Reserve’s target goal of 2% year-over-year. The question now is what the Fed will do to try to further reduce it.

Historic Trends

So, there is enough bad news and negative trends to cause many market commentators to predict a market downturn or recommend that we at least worry about a market downturn.

I don’t normally make stock market predictions but today I will. With 99% certainty, I predict a stock market crash, a Bear Market (greater than 20% decline from a previous high), is going to happen.

What I do not know is when the stock market crash will occur. It might start next week, it might start in ten years or more, or at any time in between. But it will happen, it has always happened and there is no reason to think that market cycles are a thing of the past. The only question is timing.

Another historical trend is that forecasters, market prognosticators, economists and talking heads have a terrible record of predicting market crashes and recessions. That also includes the brother-in-law or office mate who declares himself an expert on the stock markets, the economy and everything else (and yes, it is almost always a male).

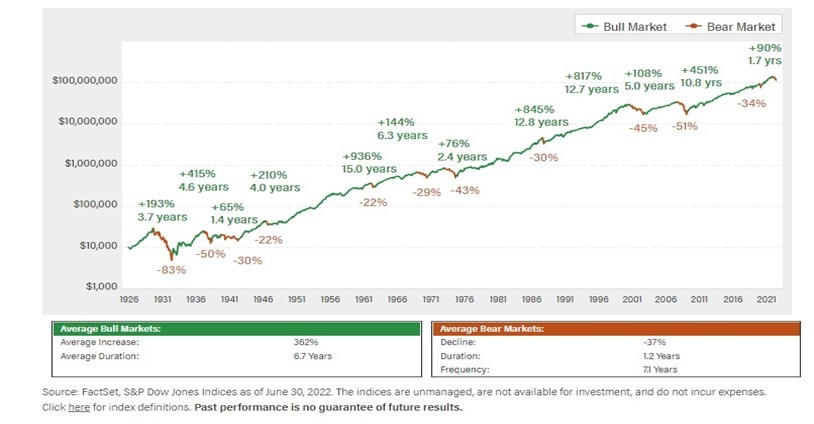

Finally, and most strikingly, declines in Bear Markets have been small compared to gains in Bull Markets (20% or greater increase compared to the previous low). For an illustrated explanation of Bull and Bear Markets, click here..

The chart below illustrates Bull Markets (green) and Bear Markets (red). During this time (1926-2022), the average Bull Market increase was ten times greater than the average Bear Market decrease and the average duration of Bull Markets was five times longer than the Bear Markets.

As a result, at my firm, we do not try to move client Portfolios in and out of the stock market in anticipation of what might happen in the future. We know that we don’t know when a market crash will occur and that, historically, investors who remained invested during Bear Market downturns were more than compensated by the subsequent Bull Markets.

Our strategy is to ignore the forecasts and only react to what has happened. When stock markets crash and a Portfolio is underweight stock investments by 5% or more, we sell bond funds and buy stock funds. When stocks outperform bonds to the point where a Portfolio is underweight bonds by 5% or more, we sell stock funds to buy bond funds.

This means that we are buying stocks funds when prices are relatively low and selling when prices are high.

Past performance is no guarantee of future performance and there is no guarantee that this strategy will be profitable. But it makes more sense to us than trying to forecast short-term market performance.

Disclaimers:

This is for educational purposes only. To learn more about the topics mentioned and if they are suitable for you, consult an appropriate professional. Tax laws can change at any time.

Any information provided in this presentation has been prepared from sources believed to be reliable but is not guaranteed and is not a complete summary or statement of all available data necessary for making an investment decision. Any information provided is for information purposes only and does not constitute a recommendation.

Arthur Stein and Arthur Stein Financial, LLC are not authorized to give legal or tax advice. For information on your specific situation, please consult your tax advisor regarding any tax implications and your attorney for legal implications. As required by the US Treasury Regulations, you should be aware that this presentation is not intended to be used and it cannot be used for the purposes of avoiding penalties under federal tax laws.

Keep in mind that:

- Past performance is no guarantee of future performance;

- Investments involve the risk of loss of principal and earnings;

- ETFs, mutual funds, money market funds, etc. are not guaranteed by the US Government, the FDIC, a bank or anyone else.

- “Average annual return” evens out variations in the actual year-to-year returns.

- ETFs, mutual funds and individual stocks and bonds fluctuate in value and there will always be times when they lose value.

- None of the information provided is necessarily relevant to anyone’s personal situation. Circumstances differ among individuals and you should not assume that these generalizations or information apply to you.

- Investments mentioned may not be suitable for all investors.

- An investment cannot be made directly into an index.